Cell Tower Lease Buyout vs Monthly Rent: The Real Math

You have a decision in front of you. A buyout firm has offered a lump sum for your cell tower lease. The number is big. Your current monthly rent is, comparatively, not big. The instinct to just take the lump sum is strong.

The short answer: The correct comparison is not “lump sum vs monthly rent.” It is “lump sum today vs net present value of future rent.” Done honestly, this calculation usually shows that fair-market buyout offers should land between 18x and 25x annual rent, and that unsolicited first offers typically come in at 10x to 15x. The difference is the gap that the math exposes. Call (720) 295-5333 for a custom analysis on your specific lease.

Most buyout decisions go wrong at the math stage. The property owner mentally compares two numbers (the lump sum on the table and the monthly rent currently deposited) and concludes that the lump sum is attractive because it represents many months of rent. That comparison misses the structural question: how does the lump sum compare with the lease’s full economic value

over its remaining term?

over its remaining term?

This post walks through the real math, step by step, using transparent assumptions that you can apply to your own situation.

Step 1: Establish the Remaining Lease Term

Start by figuring out how many years of rent the carrier or tower company is actually committed to, assuming they exercise all their renewal options. This is not the same as the initial term.

Example: a lease signed in 2015 with a 10-year initial term and four automatic 5-year renewal options has a potential total term of 30 years ending in 2045. As of 2026, that means 19 years of potential future rent, assuming all renewals are exercised. Because renewals are typically at the tenant’s discretion in well-sited leases, the practical expectation for a network-critical site is that all renewals will be exercised.

For the math, use the full term-with-renewals number unless there is a specific reason to expect early termination.

Step 2: Project the Rent Income Over the Remaining Term

Current rent times 12 gives annual rent. Apply the escalator structure to project year-by-year rent over the remaining term.

Example: $2,000 per month = $24,000 per year. With a 3% annual escalator, Year 2 rent is $24,720, Year 3 is $25,462, and so on. Over 19 years with 3% escalation, the total undiscounted rent collected is approximately $594,000.

Over the full potential 30-year term of a lease signed in 2015 with 3% escalators, total undiscounted rent is approximately $1.14 million. That total is the raw income the property owner would collect if they did not sell the lease.

Step 3: Apply Net Present Value (the Key Step Most Owners Skip)

Money today is worth more than money in the year 20 because it can be invested and earn a return. Net present value (NPV) discounts future rent back to today’s dollars using a discount rate that reflects the property owner’s alternative return on capital.

Choice of discount rate matters. A conservative discount rate (3% to 4%) yields a higher NPV and, therefore, a higher “fair buyout” number. An aggressive discount rate (8% to 10%) produces a lower NPV and a lower “fair buyout” number. Buyout firms typically use discount rates in the 7% to 10% range because their investors expect returns in that range. Property owners should use a discount rate that reflects their own realistic alternative investments, which for most households is in the 5% to 7% range.

For the example above ($24,000 starting rent, 3% escalator, 19 remaining years), the NPV at various discount rates:

- 4% discount rate: NPV is approximately $423,000

- 6% discount rate: NPV is approximately $349,000

- 8% discount rate: NPV is approximately $291,000

A fair-market buyout offer should fall within this range, typically closer to the lower end (because the buyer needs a return above their cost of capital) but not dramatically below.

Step 4: Translate NPV Into a Rent Multiple

Property owners find it easier to think in rent multiples than in NPV. The multiple is the buyout price divided by the annual rent.

In the example above, the NPV range of $291,000 to $423,000 represents multiples of 12x to 18x the starting annual rent ($24,000). But because the escalator increases rent over time, the effective multiple on current rent understates the lease’s value. A buyout firm pricing the deal at 18x current annual rent is actually paying less than half of the undiscounted future rent, even though the multiple sounds fair.

Industry benchmarks for fair-market cell tower lease buyouts:

- Well-sited leases with strong carriers: 18x to 22x annual rent

- Premium sites (multiple colocated carriers, high network importance): 22x to 28x annual rent

- Low-quality sites (weak network importance, short remaining term): 10x to 14x annual rent

Unsolicited first offers typically come in at 10x to 15x annual rent. The gap between the first offer and the fair-market target is usually the opportunity for negotiation.

Step 5: Adjust for Lease-Specific Factors

The multiple framework above is a starting point. The actual fair value of any specific lease depends on factors that adjust the multiple up or down.

Factors that increase the fair multiple:

- Multiple carriers are colocated on the structure (tenant diversification lowers buyer risk)

- Strong network importance (difficult to relocate the site if the lease ends)

- Long remaining term with favorable renewal language

- Escalator structure at or above 3% or CPI-linked

- Absence of a Right of First Refusal clause that suppresses competitive bidding

Factors that decrease the fair multiple:

- Single tenant with flexible termination rights

- Short remaining term

- Weak or capped escalator

- Restrictive property use rights for the tenant

- Environmental or zoning issues that create future risk

A qualified cell tower lease consultant evaluates each of these factors against comparable transactions and produces a site-specific fair value range. The FCC Competition and Infrastructure Policy Division publishes the macro wireless infrastructure context that shapes these valuations over time. Site-specific valuation builds on that macro context.

The Other Side of the Equation: Reasons to Take the Buyout

The math favors keeping the lease in most cases, but not every case. There are legitimate reasons to accept a buyout even at a modestly below-market price.

Estate planning and liquidity. Converting a long-term rental stream into immediate capital simplifies estate administration and allows for clean distribution among heirs. For older property owners or for estates with multiple beneficiaries, this simplification can be worth a 10% to 15% discount to strict NPV.

Material life events. Retirement, medical expenses, business liquidity needs, or a planned move can make immediate capital more valuable than long-term rent. The buyout trades future optionality for present flexibility.

Counterparty risk. If the property owner is concerned about the long-term financial health of the carrier or tower company holding the lease, accepting a buyout transfers that risk to a new counterparty. For sites with single-tenant leases from smaller or financially stressed carriers, this can be a meaningful consideration.

Concentration risk. A property owner whose net worth is significantly tied up in a single cell tower lease may prefer to diversify by converting the lease to cash.

These are all legitimate reasons. None of them changes the math. A property owner should still know the fair-market value of the lease before accepting a below-market offer, because the decision to take a discount should be made with eyes open rather than by accident.

A Worked Example

Consider a hypothetical property owner in suburban Denver. Cell tower lease signed in 2018, 25 years remaining on the term, assuming renewals are exercised. Current rent $2,500 per month ($30,000 annually) with a 3% annual escalator. Single-carrier (Verizon). Well-sited, network-important location in a coverage gap.

Undiscounted future rent over 25 years: approximately $1.08 million.

NPV at 6% discount rate: approximately $450,000.

Fair-market buyout multiple (well-sited, single tenant, good escalator): 20x to 22x annual rent, or $600,000 to $660,000.

Unsolicited first offer from a buyout firm: typically $360,000 to $450,000 (12x to 15x), framed as “over 12 years of your current rent in a single lump sum.”

Gap between first offer and fair-market target: $150,000 to $300,000. This is the value a consultant-led engagement would typically capture.

Note that the fair-market multiple exceeds the pure NPV because the market prices in future optionality (the lease can be extended, additional carriers can colocate, terms can be renegotiated favorably at future amendment cycles). Pure NPV is a conservative floor; fair-market transactions close above that floor.

When the Buyout Actually Wins

In some situations, even when the math is done correctly, the buyout is the right answer. Examples:

An estate with three heirs who disagree about long-term property strategy. Clean liquidation through a fair-market buyout avoids years of family friction. Even at a 10% to 15% discount from fair market value, the buyout is worth it for the relational simplification.

An owner nearing retirement who wants to eliminate all property management obligations and move the capital into an income-producing portfolio. The buyout, invested at a 5% yield, produces income comparable to the lease rent, with no property management overhead.

An owner facing a specific large expense (medical, education, business) where immediate capital is meaningfully more valuable than long-term rent. Here, the discount rate the owner should use for the NPV calculation is their personal rate of time preference, which may be substantially higher than 6% due to circumstances.

In each of these cases, the right framework is to first determine fair market value, then consciously decide whether to accept a discount for specific reasons. The mistake is letting the buyout firm’s first offer define what “fair” means.

Frequently Asked Questions

What discount rate should I use for my NPV calculation?

A reasonable range for most property owners is 5% to 7%. Lower if the owner has limited alternative investment options or a strong preference for long-term stability. Higher if the owner has high-return alternative investments available or significant near-term liquidity needs.

Does the math change if the lease has multiple carriers colocated?

Yes, in favor of higher buyout multiples. Multiple tenants diversify the buyer’s risk, and colocation revenues typically increase over time as carriers add equipment. Well-colocated sites command premium multiples.

What if the buyout offer includes a provision for continued rent for a few years?

This is called a partial buyout or a structured buyout. The math is the same: compare the NPV of the structured payment stream to the NPV of keeping the lease. Structured offers are often more attractive than pure lump sums when they preserve some optionality.

How do I handle tax implications?

Buyouts typically trigger capital gains tax treatment at the federal level, potentially with a state tax overlay. Continuing monthly rent is ordinary income taxed annually. The tax treatment affects the comparison and should be evaluated with a tax professional. A consultant can provide industry context; a CPA provides the specific tax analysis.

Is there ever a case where the first offer is at fair market?

Rarely. First offers are starting positions. Even reputable firms open at a number they are prepared to improve. If an unsolicited first offer arrives at fair market, pushing back for an independent review costs nothing and confirms the offer rather than damaging it.

How long does a buyout negotiation take?

Typical buyout negotiations take 60 to 120 days from engagement to closing, depending on title searches, survey requirements, and lender coordination. Simple transactions close faster.

What if I need the cash urgently?

Even with urgent cash needs, running the first offer through a quick independent review (which takes about a week) almost always produces an improved offer or a competing bid. The time investment is small relative to the potential improvement.

Should I consider selling the property with the lease instead?

Depends on the property. If the underlying real estate has substantial value independent of the cell tower lease, selling the property (with the lease as an encumbrance) may produce a better combined outcome than selling the lease alone. This analysis requires both a real estate valuation and a lease valuation.

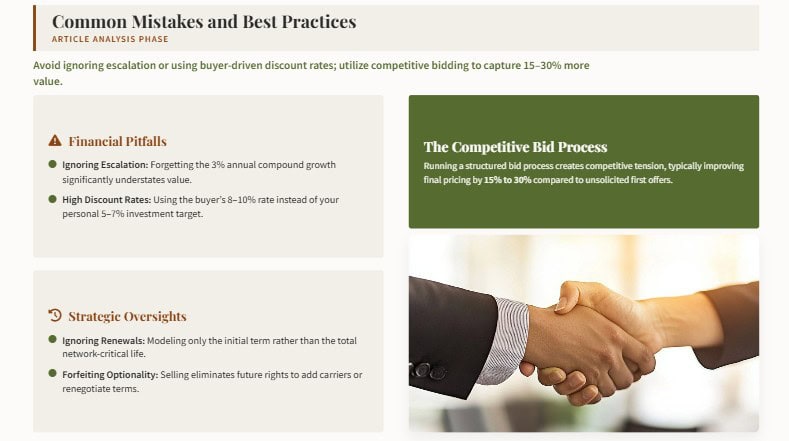

Can I get competing bids on a buyout?

Yes. A consultant can structure a competitive bid process among multiple qualified buyers. Competitive tension typically produces 15% to 30% better pricing than accepting the first unsolicited offer.

How do I get started?

Send your lease, any amendments, and any offer or buyout proposal you have received. The initial NPV analysis and valuation are part of the free consultation. Call (720) 295-5333 or use the contact page.

How to Build the Spreadsheet Yourself

A property owner who wants to run the math independently can build a simple spreadsheet with the following structure.

Column A: year number, 1 through the total remaining term (including all renewal options).

Column B: projected annual rent, calculated as the prior year’s rent times (1 + escalator rate). Start with the current rent in Year 1.

Column C: discount factor, calculated as 1 divided by (1 + discount rate) raised to the year number. Use 6% as the default discount rate unless you have reason to use a different rate.

Column D: present value of that year’s rent, calculated as Column B times Column C.

Sum Column D across all years. That sum is the lease’s net present value to you at the chosen discount rate.

Run the spreadsheet with two different discount rates (a conservative 4% and an aggressive 8%) to see the range. Fair-market buyout offers should land between those two bookends, usually closer to the aggressive end because the buyer needs a return.

The Common Mistakes to Avoid

Several mistakes are common when property owners run their own math.

Mistake 1: forgetting escalation. Using the current rent for all future years dramatically understates future value. The escalator is critical.

Mistake 2: using an excessively high discount rate. Buyout firms use 7% to 10% because their cost of capital falls within that range. Most property owners’ true alternative return is closer to 4%-6%. Using the buyout firm’s discount rate produces the buyout firm’s valuation, not yours.

Mistake 3: ignoring renewal options. The initial term is usually a fraction of the total term. If all renewals are exercised, the total term is what should be modeled. For well-sited network-critical leases, assume renewals will be exercised.

Mistake 4: forgetting future optionality. Keeping the lease preserves the option to renegotiate at each amendment cycle, add colocating tenants, or eventually sell to a buyout firm at a higher multiple after market conditions improve. Selling forfeits all of that future optionality. Market-rate buyout multiples price in optionality; pure NPV calculations do not.

Bottom Line

The buyout vs. rent decision is a math problem with an emotional overlay. Done honestly, the math reveals whether a specific offer is fair, below-market, or above-market. The emotional overlay can still tip the decision either way, but the property owner should at least know which direction they are tipping from.

Run your specific numbers before making any decision. Send your lease and any offer to a consultant for a free NPV and comparable-transaction analysis. Call (720) 295-5333 or use the contact page.

About the Author

John M. Wabiszczewicz II is the founder of JW Tower & Telecom Consulting in Denver, Colorado. Juris Doctor, Roger Williams University School of Law. Bachelor of Science in Finance, Bentley University. 5 years at American Tower, where he personally priced perpetual easement buyouts as part of the Asset Acquisitions team. 10 years at T-Mobile leading Regional Network Engineering and Real Estate for the Denver Market. The Cell Phone Tower Playbook methodology is built on 18 years of industry experience on both sides of these transactions. Firm verification: BBB profile.