Cell Tower Lease Clauses: 8 Provisions the Carrier Hopes You Miss

You are holding a 30-page document drafted by their lawyers, not yours. The cover sheet has a rent number and a term. The first page has a few friendly paragraphs. Then the pages turn into numbered sections with headings such as “Permitted Use,” “Assignment,” and “Right of First Refusal,” and the language grows denser.

The short answer: Rent is the most visible part of a cell tower lease. The clauses that silently cost the most money are the ones that almost never get discussed: the escalator structure, the Right of First Refusal, the assignment language, and five others listed below. A property owner who understands these 8 provisions before signing changes the economics of the agreement for 30 to 50 years. Call (720) 295-5333 for a free lease review.

Most property owners negotiate a cell tower lease once in their lifetime. Carriers and tower companies negotiate them every day, against teams of site acquisition specialists, real estate attorneys, and finance officers who have each closed hundreds of these deals. The asymmetry is the whole game. The 8 clauses below are where the asymmetry shows up on paper, and they are the specific sections a qualified reviewer examines line by line before anything gets signed.

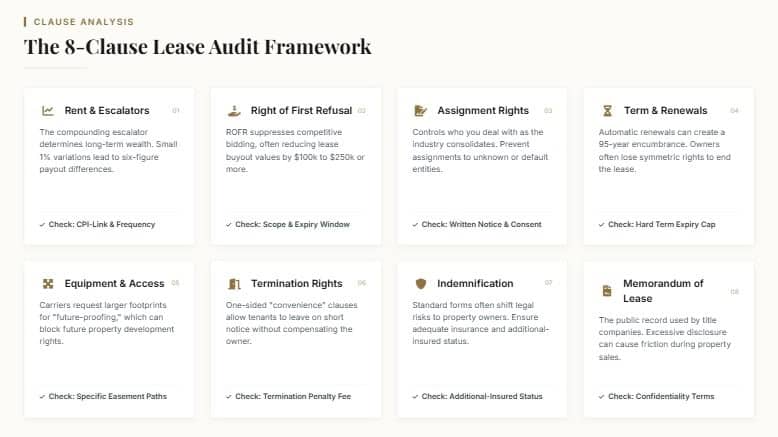

Clause 1: The Rent and the Escalator Structure

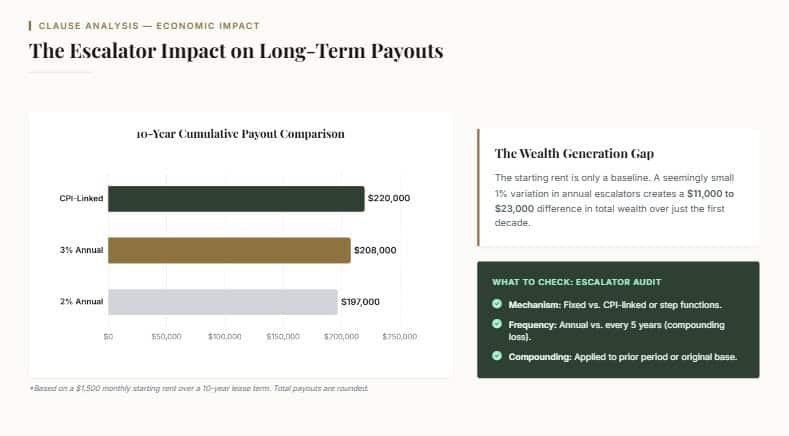

Every property owner focuses on the starting rent number because it is the easiest to see and compare. What gets missed is the escalator. A 10-year lease at $1,500 per month with a 2% annual escalator will pay out roughly $197,000 over the term. The same lease with a 3% annual escalator pays out $208,000. A CPI-linked escalator in an inflationary decade can push the term-total well above $220,000. Same starting rent, very different outcomes.

On a lease with multiple renewal options stretching the total term to 30 or 50 years, the escalator compounds. A seemingly small difference between 2% and 3% can amount to six figures over the lifetime of the agreement. The escalator deserves at least as much attention as the starting rent, and in most lease reviews, it deserves more.

What to check: the escalator mechanism (fixed percentage, CPI-linked, or step function), the frequency (annual versus every five years), the compounding method (applied to prior period’s rent or to base rent), and the cap, if any (some carriers try to cap CPI escalators at 2% or 3%, which breaks the inflation-protection purpose).

Clause 2: The Right of First Refusal

A Right of First Refusal clause gives the existing tenant (or the tower company the carrier is colocated on) the right to match any buyout offer you later receive from a third party. On its surface, this sounds reasonable. In practice, it reduces the lease’s buyout value by a structural amount that most property owners never see.

The mechanism is simple. Third-party buyout firms invest time and money evaluating your lease, running comps, and structuring an offer. If they know their offer can be matched by the existing tenant, they have no incentive to offer a top-of-market price. Why would anyone expend the effort on a competitive bid that will be matched and awarded to someone else? The answer is: they mostly do not. The presence of an ROFR clause suppresses the competitive bidding that drives buyout prices up.

On a typical mid-market cell tower lease, a ROFR clause can reduce buyout value by $100,000 or more. On a seven-figure lease, the reduction can exceed $250,000. The clause is often buried in a section titled “Purchase Options” or “Transfer of Interests” and is easy to miss on a fast read.

What to check: whether a ROFR clause exists at all, what it applies to (buyouts only, or also sales of the property itself), and how narrowly or broadly it is drafted. A skilled reviewer will recommend either removal of the clause or a tightly drafted version that applies only to identical offers and expires within a short window.

Clause 3: The Assignment Rights

Assignment language controls what the tenant can do with the lease without your consent. Most standard carrier leases permit the tenant to assign the lease freely to affiliates, successor entities, and third-party purchasers. That means the counterparty you sign with today may not be the counterparty you deal with in five years.

This matters more than most property owners realize. The cell tower industry has seen significant consolidation over the past 15 years. Leases originally signed with small tower companies have been sold to larger entities in waves. Leases originally signed with one of the major carriers have been assigned to tower companies, then to other tower companies, then to specialty infrastructure funds. The counterparty you trusted when you signed may not be the one who returns your calls when you need to negotiate an amendment.

The fix is not to prohibit assignment, which would break the deal entirely because carriers and tower companies need liquidity in their lease portfolios. The fix is to require notice of any assignment, prohibit assignment to entities in default on any obligation under the lease, and ensure that any assignee expressly assumes in writing all obligations of the original tenant. This is usually negotiable and always worth negotiating.

Clause 4: The Term and Renewal Option Structure

A cell tower lease is never really a 10-year agreement. The standard structure is a short initial term (5 or 10 years) with multiple automatic renewal options under the tenant’s control. A lease written as “10-year term with four automatic 5-year renewal options” is effectively a 30-year lease, with the tenant retaining the decision rights on renewal. If the tenant wants to extend, they extend. If they want to terminate, they terminate. The property owner has no symmetric right.

JW Tower has seen leases structured for 50, 75, and even 95 years of potential tenant-controlled term. That is not a lease. That is a near-permanent encumbrance on the property’s development rights.

What to check: the initial term length, the number and length of renewal options, which party controls each renewal decision, the notice requirements for exercising or declining renewals, and any termination rights for either party during the term. A skilled reviewer will push for symmetric renewal rights (either party can end the relationship at the end of a defined period) or a hard term cap beyond which the lease expires, regardless of the other.

Clause 5: The Equipment Area and Access Easements

Cell tower leases typically specify a “premises” or “equipment area” along with access easements across the rest of the property to reach that area. Carriers and tower companies routinely request premises and easements larger than their current equipment actually requires. The reasoning is “future-proofing”: they want room to add equipment without having to renegotiate.

The property owner’s interest runs in the opposite direction. A smaller, more tightly defined premises protects the rest of the property from encroachment. A more narrowly drawn access easement preserves the property owner’s ability to develop, landscape, or sell adjacent land. A specific location for utility easements (electrical, fiber) prevents the property owner from discovering in year 12 that the carrier ran a conduit through what is now the footprint of a planned building.

What to check: the exact square footage of the equipment area, the width and location of the access easement, the specific utility corridors, and any future expansion language. If the lease allows the tenant to expand the equipment area at their discretion, the property owner has effectively given up control of a portion of the property.

Clause 6: The Termination for Convenience Language

Many cell tower leases grant the tenant broad termination rights. The carrier can terminate the lease on 30, 60, or 90 days’ notice at any time and for any reason (or no reason at all). The property owner has no equivalent right. This is structurally unbalanced and usually negotiable.

The tenant’s argument for broad termination rights is that the network needs to change. A site that is critical in 2026 may be redundant in 2030 as network topology evolves. That is a fair argument. The counter-argument is that the property owner has no control over network planning and should not bear the entire risk of a tenant-initiated termination without any compensation.

What to check: the termination notice period, the reasons for termination (if any are specified), and whether any termination fee or residual payment is triggered. A skilled reviewer will push for either a termination fee tied to the remaining term’s net present value, a reduction in the tenant’s termination rights (limiting them to material network changes rather than discretion), or a matching termination right for the property owner.

Clause 7: The Indemnification and Insurance Provisions

This is where the legal risk lives. Cell tower leases routinely require the property owner to indemnify the tenant against broad categories of claims, while the tenant provides narrow indemnification in return. The property owner ends up bearing more risk than the tenant in a one-sided exchange.

Insurance requirements are a related concern. The tenant carries insurance on their equipment and their operations. The property owner needs to confirm that the tenant’s insurance is adequate and that the property owner is named as an additional insured on the relevant policies. Many standard leases do not automatically grant additional-insured status, and the property owner has to negotiate for it.

What to check: the scope of each party’s indemnification, the exceptions and carve-outs, the insurance limits, the additional-insured language, and the handling of subrogation rights. This is one area where a real estate attorney’s legal review adds specific value alongside the cell tower lease consultant’s business review.

Clause 8: The Memorandum of Lease and Recording

Cell tower leases are typically accompanied by a shorter document called a Memorandum of Lease or Memorandum of Ground Lease, which gets recorded in the county land records. The property owner signs this alongside the main lease. The Memorandum creates a public record of the tenant’s interest in the property.

The concern is what the Memorandum includes. Some standard Memoranda broadly describe the tenant’s rights, including renewal options and even assignment rights. Others are narrower, describing only the basic fact of the lease and leaving the specific rights to the underlying unrecorded agreement. The difference matters when the property is later sold or refinanced: the recorded Memorandum is what a title company and a future buyer will see, and broad Memorandum language can create friction in those later transactions.

What to check: the exact text of the Memorandum, whether the underlying unrecorded lease is referenced in a way that makes its terms relevant to future buyers, and whether any confidentiality provisions in the main lease are undermined by disclosures in the Memorandum.

The Meta-Clause: How These Eight Work Together

The eight clauses above are not independent. They interact. A permissive assignment clause combined with a broad termination-for-convenience right means the tenant can assign the lease to a shell entity and then terminate. A ROFR clause combined with a long renewal option structure artificially suppresses any future buyout for 30 years. A large equipment area, combined with broad indemnification, shifts both the physical footprint and the financial risk to the property owner simultaneously.

A qualified reviewer reads these clauses together, not independently. The question is not just “is this provision acceptable on its own” but “what happens when this provision interacts with the other seven.” That is the value a cell tower lease consultant with operational experience brings to a lease review.

For context on how the wireless industry’s economic structure shapes these clauses, the U.S. FCC’s Competition and Infrastructure Policy Division publishes policy materials that explain why carriers ask for the clause structures they do. This is useful reading before any lease negotiation.

How JW Tower & Telecom Consulting Reviews a Lease

The firm’s process runs a lease through a structured review of each of the 8 clauses above, plus 12 additional provisions that are less frequent but occasionally appear in non-standard agreements. The output is a written assessment that identifies the specific changes the property owner should negotiate for, the economic impact of each change, and the likelihood the carrier will accept each proposed change based on how their internal approval process works.

Founder John M. Wabiszczewicz II spent 15 years inside the industry before founding the firm. At American Tower, he drafted and approved lease language as an Asset Acquisitions Attorney. At T-Mobile, he led Regional Network Engineering and Real Estate across six states, which meant sitting in the chair where clause changes were evaluated and approved. He knows which clauses are genuinely non-negotiable from the carrier’s side and which ones will move with the right counterproposal.

This is The Cell Phone Tower Playbook: the firm’s named methodology that covers Free Consultation, Document & Site Review, Strategy & Negotiation Plan, Representation Through Closing, and Ongoing Support.

Frequently Asked Questions

How long does a full lease review take?

A standard cell tower lease runs 25 to 60 pages. A full review takes 3 to 5 business days. An expedited review for a time-sensitive offer can be done in 48 to 72 hours. The initial conversation about whether a full review makes sense usually takes 30 to 60 minutes.

Which clause matters most?

On most leases, the escalator structure and the Right of First Refusal clause are the two with the biggest long-term economic impact. These should always be examined carefully. The other six clauses matter, but the rank order varies depending on the specific lease and the property owner’s circumstances.

Are carrier standard forms negotiable?

Yes. Carriers and tower companies present their standard forms to standardize costs and risk exposure across thousands of sites. “Standard” is not a synonym for “unchangeable.” Roughly 80% of the clauses in a standard form can be modified with the right counterproposal, particularly for sites the carrier genuinely needs in their network.

What if I already signed a lease with bad terms?

The lease is not unchangeable. Most cell tower leases have built-in amendment cycles (when the carrier adds equipment, renews the term, or requests operational changes). Each amendment cycle is an opportunity to rebalance terms that were unfavorable in the original agreement. A consultant can build a multi-year strategy to improve the lease’s terms at the next amendment trigger.

Does the carrier have to accept my proposed changes?

No. The carrier has its own risk tolerance and its own internal approval process. What a skilled consultant does is frame the proposed changes in language that the carrier’s internal process will accept. A change that appears to be a concession to the carrier is easier to approve than one that appears to be a landowner power grab, even when the economic effect is the same.

What if the offer has a tight deadline?

Deadlines on cell tower lease offers are almost always negotiation tactics rather than real operational deadlines. A consultant can usually extend the deadline by directly engaging with the carrier and requesting additional time. Carriers prefer to deal with represented property owners because the process moves more efficiently. The pressure of the stated deadline is not a real constraint in most cases.

Do I need a full review if I just want a second opinion?

A second-opinion review is a common and useful engagement. It takes less time than a full negotiation and produces a written assessment that the property owner can use to decide whether to accept the existing offer, negotiate specific changes, or seek a more aggressive outcome. Success fees scale with engagement, so a second-opinion review that confirms the offer is fair incurs no fee.

Can I use this 8-clause checklist myself?

Yes, for an initial read. The list above tells you what to look for. What the list does not give you is the market data to evaluate whether the terms you find are favorable, average, or below-market. That requires access to comparable leases in your county and operational knowledge of how carriers structure their deals. A self-review identifies the questions. A consultant provides the answers.

What about the language carriers called “boilerplate”?

Boilerplate is a marketing word. The sections carriers describe as boilerplate often contain the provisions that have the greatest long-term economic impact. Do not skip a clause because someone called it standard.

How do I get started?

Send a copy of your current lease and any amendments. The initial consultation is free. Call (720) 295-5333 or use the contact page to book a review.

Bottom Line

A cell tower lease is a long-term document with a lot of quiet economic machinery inside it. Rent is the obvious part. The 8 clauses above determine the lifetime value. A property owner who understands these provisions before signing changes the economics of the agreement for the next 30 to 50 years.

For a free lease review against this 8-clause framework, call (720) 295-5333 or reach out through the contact page. For more on why rent is not the most important variable, see our post on why lease terms matter more than rent.

About the Author

John M. Wabiszczewicz II is the founder of JW Tower & Telecom Consulting in Denver, Colorado. He holds a Juris Doctor from Roger Williams University School of Law and a Bachelor of Science in Finance from Bentley University. He spent 5 years at American Tower (as an Asset Acquisitions Attorney and Tower Acquisitions Representative) and 10 years at T-Mobile (leading Regional Network Engineering and Real Estate for the Denver Market across 6 states). He founded JW Tower & Telecom Consulting to represent property owners, drawing on the insider knowledge he had previously applied on the carrier side. Firm verification: BBB profile.